|

The Week Ahead: Highlights

US Preview

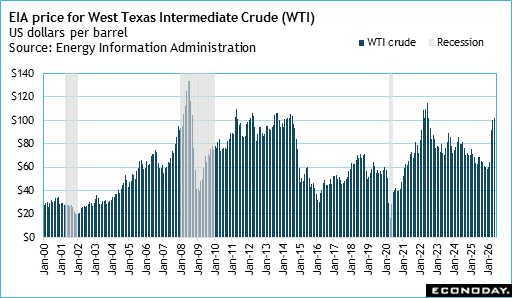

Watching for Energy Price Impact on CPI, PPI

By Theresa Sheehan, Econoday Economist

The June 8 week includes two of the earliest reports related

to inflation in May. The consumer price index (CPI) is at 8:30 ET on Wednesday

and the final demand producer price index (PPI) is at 8:30 ET on Thursday. The

former will provide information about how much pass-through to consumer prices

has occurred after energy prices spiked in March and remained elevated into

April, and how much more price pressure remains at the producer level. While

the initial big run up in energy prices that started in March is over, energy

prices remain elevated. Signs of a meaningful decline in oil prices are absent

as tentative dips are being erased amid chaotic messages about the state of the

war on Iran.

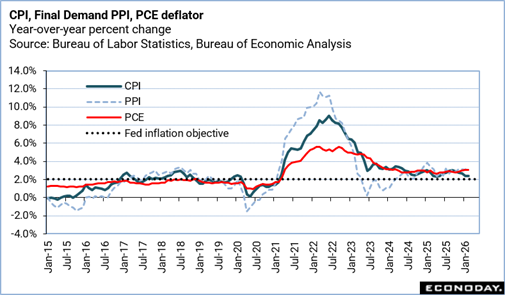

The substantial month-over-month increase in the CPI in

April from March for food and beverages (up 0.5 percent) and energy (up 3.8

percent) drove much, but not all, of the 0.6 percent rise at the all-items

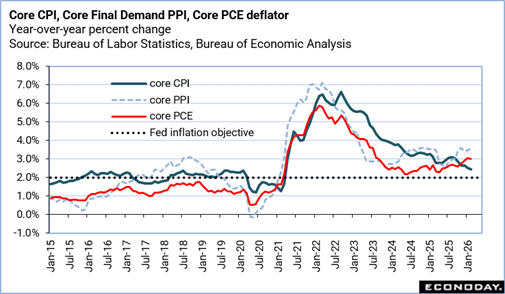

level. The core CPI in April was up 0.4 percent from the prior month. While the

pace of increases in the overall CPI moderated a bit in April, the pace at the

core accelerated. Goods prices are being pushed higher by rising transportation

costs which are not yet coming down and will likely remain elevated for at

least a few more months.

The April PPI should show less upward pressure on prices

from energy costs. The month-over-month gain of 1.4 percent in final demand in

April probably was the peak that reflects the rise in oil prices. The monthly

increase for the core PPI excluding food, energy, and trade services was

0.6 percent in April.

What Fed policymakers will be more attentive to will be the

annual pace of increases rather than potentially volatile month-to-month

changes. The all-items CPI was up five-tenths to up 3.8 percent in April while

the core CPI was up two-tenths to up 2.8 percent. Consumer price inflation has

been moving in the wrong direction for two months now. The year-over-year

increase in the PPI jumped to 6. Percent in April after rising to 4.3 percent

in March from 3.4 in February. The core PPI reached a 4.4 percent increase in

April after 3.7 percent in March. Producers of goods and services are seeing

input costs rising rapidly and substantially, and will be passing some of that

on to customers.

The FOMC next meets on June 16-17. The communications

blackout period around the meeting will go into effect at midnight on Saturday,

June 6 and run through midnight on Thursday, June 18. Whatever the inflation

reports say about price stability, there will be no public comment on it from

monetary policymakers.

The Week Ahead: Econoday Consensus Forecasts

Monday

Japan GDP for First Quarter (Mon 0850 JST; Sun 2350

GMT; Sun 1950 EDT)

Consensus Forecast, Q/Q: 0.3%

Consensus Range, Q/Q: 0.2% to 0.5%

Consensus Forecast, Annualized 1.3%

Consensus Range, Annualized: 1.0% to 2.0%

Japan's revised gross domestic product for the January-March

quarter is expected to

be revised downward from the preliminary reading, mainly

dragged down by weaker

corporate capital expenditure.

The January-March GDP is expected to be revised down to a

0.3 percent rise on the quarter

from the preliminary estimate of a 0.5 percent rise released

on May 19. On an annualized

basis, the revised GDP is forecast to show a 1.3 percent

increase, slowing from the initial

reading of a 2.1 percent gain. Compared with a year earlier,

the economy is projected to

expand 0.3 percent, down from the preliminary result of a

0.6 percent increase.

Germany Manufacturing Orders for April (Mon 0800 CEST;

Mon 0600 GMT; Mon 0200 EST)

Consensus Forecast, M/M: -2.0%

Consensus Range, M/M: -3.5% to 1%

Consensus Forecast, Y/Y: 4.8%

Consensus Range, Y/Y: 4.3% to 4.9%

Orders expected to retreat by 2.0 percent on the month in

April after rising 5.0 percent in March.

Tuesday

South Korea GDP for First Quarter (Tue 0800 KST; Mon

2300 GMT; Mon 1900 EDT)

Consensus Forecast, M/M: 1.7%

Consensus Range, M/M: 1.7% to 1.7%

Consensus Forecast, Y/Y: 3.6%

Consensus Range, Y/Y: 3.6% to 3.6%

The consensus sees GDP growth at 1.7 percent on quarter and 3.6

percent on year, unchanged from the last report.

China Merchandise Trade Balance for May (Anytime)

Consensus Trade Balance Forecast: $88.6B

Consensus Trade Balance Range: $86.2B to $88.8B

The surplus is expected to widen slightly to $88.6 billion

from $84.8 billion in April.

Germany Industrial Production for April (Tue 0800

CEST; Tue 0600 GMT; Tue 0200 EDT)

Consensus Forecast, M/M: -0.2%

Consensus Range, M/M: -0.5% to 0.8%

Consensus Forecast, Y/Y: -1.5%

Consensus Range, Y/Y: -1.8% to -1.0%

Germany remains in a funk with output seen eroding again by

0.2 percent on month in April after decreasing by 0.5 percent in March. On

year, the decline is expected to narrow to 1.5 percent after falling by 3.0

percent in March from last year.

Germany Merchandise Trade for April (Tue 0800 CEST; Tue

0600 GMT; Tue 0200 EDT)

Consensus Forecast, Balance: E16.5 B

Consensus Range, Balance: E13.6 B to E17.0 B

The consensus sees the surplus widening to E16.5 billion in

April from E14.3 billion in March.

US NFIB Small Business Optimism Index for May (Tue

0600 EDT; Tue 1000 GMT)

Consensus Forecast, Index: 96.1

Consensus Range, Index: 95.7 to 97.0

Forecasters see the index edging up to 96.1 in May from 95.9

in April as sentiment remains subdued amid worries about surging fuel prices.

Canada Merchandise Trade for April (Tue 0830 EDT; Tue

1230 GMT)

Consensus Forecast, Balance: C$2.3 B

Consensus Range, Balance: C$1.5 B to C$2.7 B

High oil prices flatter exports to lift the surplus to C$2.3

billion from C$1.8 billion in March.

US International Trade in Goods and Services for April (Tue

0830 EDT; Tue 1230 GMT)

Consensus Forecast, Balance: -$55.5 B

Consensus Range, Balance: -$57.9 B to -$54.0B

The deficit is expected to narrow to $55.5 billion in April

from $60.3 billion in March. Imports expected to slow after big gains in March

while higher prices for energy products help on the export side.

US Existing Home Sales for May (Tue 1000 EDT; Tue 1400

GMT)

Consensus Forecast, Annual Rate: 4.08 M

Consensus Range, Annual Rate: 4.04 M to 4.10 M

Seen marginally higher at a 4.08 million unit rate in May versus

4.02 million in April as sales remain depressed with mortgage rates ticking up.

Wednesday

Japan PPI for May (Wed 0850 JST; Tue 2350 GMT; Tue 1930

EDT)

Consensus Forecast, M/M: 0.7%

Consensus Range, M/M: 0.4% to 1.2%

Consensus Forecast, Y/Y: 5.6%

Consensus Range, Y/Y: 5.4% to 6.2%

Japan's producer inflation, measured by the corporate goods

price index (CGPI), is

expected to top 5 percent on the year in May, accelerating

at the fastest pace in three years.

The CGPI is seen to have picked up momentum as geopolitical

tensions in the

Middle East continue to push up prices of oil products and

other raw materials, with the

impact spreading to oil-derived products such as chemicals.

Coupled with the weakness of the yen, which is pushing up

import costs, the CGPI is

expected to rise 5.6 percent on the year in May, the highest

since April 2023 when it hit 6.1 percent.

The index surged unexpectedly to 4.9 percent in April,

outpacing the market forecast of 3.2 percent. On a month-on-month basis, the

CGPI is expected to rise for the third straight month,

rising 0.7 percent in May after jumping 2.3 percent in

April, when price increases in oil products,

chemical products, utilities, non-ferrous metals, as well as

food and beverages led the

gains.

China CPI for May (Wed 0930 CST; Wed 0130 GMT; Tue

2130 EDT)

Consensus Forecast, Y/Y: 1.3%

Consensus Range, Y/Y: 1.2% to 1.4%

CPI expected to edge up to 1.3 percent on year in May from a

subdued 1.2 percent in April.

China PPI for May (Wed 0930 CST; Wed 0130 GMT; Tue

2130 EDT)

Consensus Forecast, Y/Y: 3.8%

Consensus Range, Y/Y: 3.0% to 4.0%

Producer prices picking up steam with the consensus looking

for PPI up 3.8 percent on year in May after 2.8 percent in April, with a big

boost from commodities prices linked to rising energy prices.

Italy Industrial Production for April (Wed 1000 CEST;

Wed 0800 GMT; Wed 0400 EDT)

Consensus Forecast, M/M: 0.1%

Consensus Range, M/M: -0.1% to 0.2%

Consensus Forecast, Y/Y: 0.5%

Consensus Range, Y/Y: 0.4% to 1.1%

The consensus sees output up 0.1 percent on month and 0.5

percent on year in April after rising 0.7 percent on the month and 1.5 percent

on year in March.

US CPI for May (Thu 0830 EDT; Thu 1230 GMT)

Consensus Forecast, CPI - M/M: 0.5%

Consensus Range, CPI - M/M: 0.3% to 0.7%

Consensus Forecast, CPI - Y/Y: 4.2%

Consensus Range, CPI - Y/Y: 3.9% to 4.3%

Consensus Forecast, Ex-Food & Energy - M/M: 0.3%

Consensus Range, Ex-Food & Energy - M/M: 0.2% to

0.5%

Consensus Forecast, Ex-Food & Energy - Y/Y: 2.9%

Consensus Range, Ex-Food & Energy - Y/Y: 2.8% to 3.0%

CPI seen up 0.5 percent on the month and 4.2 percent on year

as energy prices lift the total. Core CPI expected at 0.3 percent and 2.9

percent, respectively. Lots of components expected to show the impact of higher

energy costs including food, housing, fertilizer, chemicals, metals, and more.

Canada Bank of Canada Announcement (Wed 0945 EDT; Wed

1345 GMT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Level: 2.25%

Consensus Range, Level: 2.25% to 2.25%

Bank of Canada expected to lean dovish and push back on

market expectations for a rate hike by holding rates steady.

Thursday

Eurozone ECB Announcement (Thu 1415 CEST; Thu 1215

GMT; Thu 0815 EDT)

Consensus Forecast, Refi Rate Change: 25 bp

Consensus Range, Refi Rate Change: 25 bp to 25 bp

Consensus Forecast, Refi Rate Level: 2.40%

Consensus Range, Refi Rate Level: 2.40% to 2.40%

Consensus Forecast, Deposit Rate Change: 25 bp

Consensus Range, Deposit Rate Change: 25 bp to 25 bp

Consensus Forecast, Deposit Rate Level: 2.25%

Consensus Range, Deposit Rate Level: 2.25% to 2.25%

After a series of hawkish statements from ECB officials,

forecasters uniformly expect a 25 basis point rate increase as the bank seeks

to head off an inflation spurt due to rising fuel costs.

US Jobless Claims for Week of June 11 (Thu 0830 EDT;

Thu 1230 GMT)

Consensus Forecast, Initial Claims - Level: 218 K

Consensus Range, Initial Claims - Level: 215 K to 227

K

Claims to recede to 218K, down toward the 4-week moving

average of 214.75K, after an unexpected jump of 13K last week to 225K. Most

observers see the employment market as basically in balance and showing

stability given headwinds now including surging energy costs.

US PPI-Final Demand for May (Thu 0830 EDT; Thu 1230

GMT)

Consensus Forecast, PPI-FD - M/M: 0.7%

Consensus Range, PPI-FD - M/M: 0.4% to 0.9%

Consensus Forecast, PPI - Y/Y: 6.4%

Consensus Range, PPI - Y/Y: 6.3% to 6.8%

Consensus Forecast, Ex-Food & Energy - M/M: 0.4%

Consensus Range, Ex-Food & Energy - M/M: 0.3% to 0.5%

Another nasty inflation reading largely due to rising fuel

costs. The consensus sees PPI-FD up 0.7 percent on the month and 6.4 percent

on year in May, shocking numbers. Excluding food & energy, the call is up

0.4 percent on the month.

Friday

Germany CPI for May (Fri 0800 CEST; Fri 0600 GMT; Fri

0200 EDT)

Consensus Forecast, M/M: -0.2%

Consensus Range, M/M: -0.2% to -0.2%

Consensus Forecast, Y/Y: 2.6%

Consensus Range, Y/Y: 2.6% to 2.6%

Consensus Forecast, HICP - M/M: -0.1%

Consensus Range, HICP - M/M: -0.1% to -0.1%

Consensus Forecast, HICP - Y/Y: 2.7%

Consensus Range, HICP - Y/Y: 2.7% to 2.7%

The consensus sees no revision in the final from the flash

with CPI down 0.2 percent on the month and up 2.6 percent on year.

UK Monthly GDP for April (Fri 0700 BST; Fri 0600 GMT;

Fri 0200 EDT)

Consensus Forecast, M/M: -0.1%

Consensus Range, M/M: -0.2% to 0.1%

Forecasters see GDP down 0.1 percent on the month in April

after a strong 0.3 percent increase in March.

France CPI for May (Fri 0845 CEST; Fri 0645 GMT; Fri

0245 EDT)

Consensus Forecast, M/M: 0.1%

Consensus Range, M/M: 0.1% to 0.1%

Consensus Forecast, Y/Y: 2.4%

Consensus Range, Y/Y: 2.4% to 2.4%

Consensus Forecast, HICP - M/M: 0.1%

Consensus Range, HICP - M/M: 0.1% to 0.1%

Consensus Forecast, HICP - Y/Y: 2.8%

Consensus Range, HICP - Y/Y: 2.8% to 2.8%

The consensus sees no revision in the final from the flash

with CPI up 0.1 percent on the month and up 2.4 percent on year.

India CPI for May (Fri 1600 IST; Fri 1030 GMT; Fri 0630

EDT)

Consensus Forecast, Y/Y: 4.0%

Consensus Range, Y/Y: 3.5% to 4.1%

Inflation expected at 4.00 percent on year in May, up from

3.48 percent in April.

US Consumer Sentiment for June (Fri 1000 EDT; Fri 1400

GMT)

Consensus Forecast, Index: 46.1

Consensus Range, Index: 45.0 to 48.5

The consensus sees a bit of a rebound to 46.1 in June from

May's extraordinarily low 44.8 but that is a very low reading reflecting a very

gloomy consumer focused on surging living costs and rising inflation

expectations.

|

![[Apple App Store]](/images/AppleAppStore.png)

![[Econoday on Kindle]](/images/kindle.jpg)