|

The Week Ahead: Highlights

Asia-Pacific Preview

Markets Eye Australia Data after RBA Keeps Rates

Unchanged

By Brian Jackson, Econoday Economist

Key Australian data will be the focus of the Asia-Pacific

data calendar in the week ahead after the Reserve Bank of Australia left policy

rates on hold this week. The monthly inflation report for June will be watched

particularly closely after last month's report showed inflation above the RBA's

target range of two percent to three percent for the ninth consecutive month.

The RBA expressed its confidence that the three rate hikes already delivered so

far this year will eventually help to bring inflation back into the target

range but a high inflation number next week will likely boost the chances for

further policy tightening.

Australian labor market and household spending data will

also be assessed in light of the RBA's decision this week. Last month's reports

showed weaker spending and an increase in the unemployment rate, with the

impact of the Iran conflict on fuel prices and sentiment having a notable

impact on the data.

The People's Bank of China will hold its monthly review of

the loan prime rates next week. These rates have been on hold since May 2025

and officials provided little indication that a shift in policy settings is

being considered when monthly activity data were published this week. Officials

characterised the data as showing the economy has "maintained steady

momentum" but again cautioned that the external environment is "complex

and volatile".

Singapore and Hong Kong data next week will be watched for

any sign that the impact of the Iran conflict is easing, with both

reporting inflation data, Singapore reporting industrial production data, and

Hong Kong reporting trade data. The flash PMI survey for India will provide an

early indication of conditions in June.

US Preview

Personal income, Spending PCE Price Indexes in Focus

after FOMC Meeting

By Theresa Sheehan, Econoday Economist

The June 22 week has a busy data schedule. However, in the

wake of the June 16-17 FOMC meeting, the standout report is likely to be the

May numbers on personal income and spending and the PCE deflator at 8:30 ET on

Thursday.

Although all the job market data is in aggregate in good

balance for supply and demand, the reality is that only a few narrow sectors

are consistently hiring and offering competitive wages. For most households,

income is more-or-less flat. This contrasts with rising consumer spending that

is largely related to sharp increases in energy costs directly in the form of

gasoline and home heating/cooling and indirectly in food and services prices.

Households are shifting away from discretionary spending and/or buying more on

credit out of necessity.

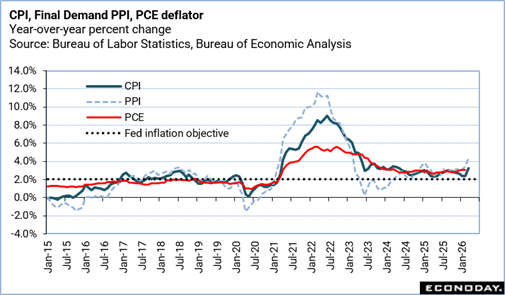

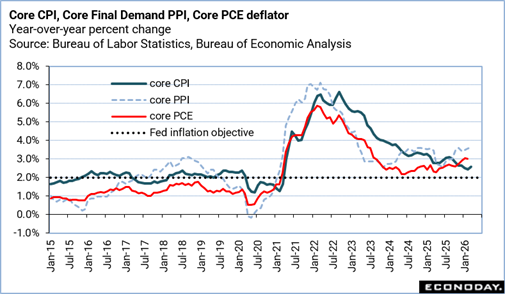

The PCE deflator in April was up 3.8 percent compared to a

year earlier, an increase of three-tenths from the prior month. However, the

core PCE deflator was up only one-tenth to up 3.3% from April 2025 and the PCE

deflator excluding food, energy, and shelter was up 3.3% in April the same as

in March.

The May data will tell the story about whether incomes are

struggling to keep up with spending, and if some of the previous upward price

pressures at the producer level are working into core prices.

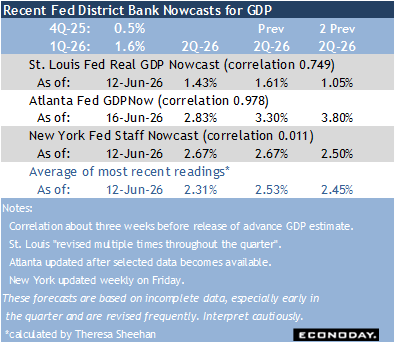

The final read on first quarter GDP is at 8:30 ET on

Thursday may see a little upward revision but will not be meaningfully changed

from the up 1.6 percent in the second estimate. At this date the second quarter

is already nearing an end. Policymakers' focus will be on the advance estimate

of second quarter GDP at 8:30 ET on Thursday, July 30. GDP forecasts from the

St. Louis, New York, and Atlanta Feds all point to faster growth in the second

quarter. The estimates average to an increase of about 2.3 percent, about the

Fed's longer-run expectation of 2 percent.

The Week Ahead: Econoday Consensus Forecasts

Monday

China Loan Prime Rate for June (Mon 0915 CST; Mon

0115 GMT; Sun 2115 EDT)

Consensus Forecast, 1-Year Rate - Change: 0 bp

Consensus Range, 1-Year Rate - Change: 0 bp to 0 bp

Consensus Forecast, 1-Year Rate - Level: 3.0%

Consensus Range, 1-Year Rate - Level: 3.0% to 3.0%

Consensus Forecast, 5-Year Rate - Change: 0 bp

Consensus Range, 5-Year Rate - Change: 0 bp to 0 bp

Consensus Forecast, 5-Year Rate - Level: 3.50%

Consensus Range, 5-Year Rate - Level: 3.50% to 3.50%

Forecasters see no change again in LPR as there has been no

signal from the PBOC and authorities choose to rely on fiscal tools to boost

the flagging economy.

Canada CPI for May (Mon 0830 EDT; Mon 1230 GMT)

Consensus Forecast, CPI - M/M: 0.8%

Consensus Range, CPI - M/M: 0.6% to 0.8%

Consensus Forecast, CPI - Y/Y: 3.0%

Consensus Range, CPI - Y/Y: 2.9% to 3.1%

Energy prices are seen as the culprit along with food in

lifting inflation with expectations calling for an annual increase to 3.0

percent in May, up from 2.8 percent in April.

Eurozone EC Consumer Confidence Flash for June (Mon

1600 CEST; Mon 1400 GMT; Mon 1200 EDT)

Consensus Forecast, Index: -17.5

Consensus Range, Index: -18.0 to -16.0

Sentiment expected higher at minus 17.5 for June compared

with minus 19.0 in May.

Tuesday

Singapore CPI for May (Tue 1300 SGT; Tue 0500 GMT; Tue

0100 EDT)

Consensus Forecast, Y/Y: 2.0%

Consensus Range, Y/Y: 1.9% to 2.1%

CPI seen slightly higher at 2.0 percent on year for May

versus 1.8 percent in April, a remarkably low figure given energy price

pressures.

France PMI Composite Flash for June (Tue 0815 CEST;

Tue 0615 GMT; Tue 0215 EDT)

Consensus Forecast, Composite Index: 45.6

Consensus Range, Composite Index: 45.1 to 46.0

Consensus Forecast, Manufacturing Index: 49.8

Consensus Range, Manufacturing Index: 49.6 to 50.5

Consensus Forecast, Services Index: 45.8

Consensus Range, Services Index: 44.0 to 46.8

Slightly better but still showing substantial contraction

with services lagging badly. The composite is seen at 45.6 for the June flash

versus 44.9 in the May final.

Germany PMI Composite Flash for June (Tue 0930 CEST;

Tue 0730 GMT; Tue 0330 EDT)

Consensus Forecast, Composite Index: 49.3

Consensus Range, Composite Index: 47.9 to 50.0

Consensus Forecast, Manufacturing Index: 50.3

Consensus Range, Manufacturing Index: 49.0 to 50.8

Consensus Forecast, Services Index: 48.5

Consensus Range, Services Index: 46.0 to 49.5

The consensus sees business activity edging up to a nearly

flat showing (50 is neutral) with manufacturing showing a very modest

expansion. The consensus sees the composite at 49.3 for June flash versus 48.8

in the May final. Manufacturing expected at 50.3 versus 50.1 in May final.

Eurozone PMI Composite Flash for June (Tue 0930 CEST;

Tue 0730 GMT; Tue 0330 EDT)

Consensus Forecast, Composite Index: 48.7

Consensus Range, Composite Index: 48.0 to 49.1

Consensus Forecast, Manufacturing Index: 51.5

Consensus Range, Manufacturing Index: 50.5 to 52.3

Consensus Forecast, Services Index: 48.4

Consensus Range, Services Index: 46.0 to 49.3

Pretty much no change is the call with the composite

expected at 48.7 in the June flash versus 48.5 in the May final. Manufacturing

expected in expansion again at 51.5 for the June flash versus 51.6 in the May

final. Services seen at 48.4 in June flash versus 47.7 in. the May final.

UK PMI Composite Flash for June (Tue 0930 BST; Tue 0830

GMT; Tue 0430 EDT)

Consensus Forecast, Composite Index: 49.8

Consensus Range, Composite Index: 49.1 to 50.5

Consensus Forecast, Manufacturing Index: 53.5

Consensus Range, Manufacturing Index: 53.4 to 53.5

Consensus Forecast, Services Index: 50.0

Consensus Range, Services Index: 49.0 to 50.1

Composite expected at 49.8 in the June flash versus 49.7 in

the May final. Manufacturing stays strong, expected at 53.5 versus 53.9 and

services at 50.0 versus 49.3.

US PMI Composite Flash for June (Tue 0945 EDT; Tue

1345 GMT)

Consensus Forecast, Composite Index: 51.2

Consensus Range, Composite Index: 50.6 to 52.1

Consensus Forecast, Manufacturing Index: 54.6

Consensus Range, Manufacturing Index: 54.5 to 55.3

Consensus Forecast, Services Index: 51.0

Consensus Range, Services Index: 50.4 to 51.3

Another month of modest expansion is the call. Composite

expected at 51.2 for the June flash versus 51.5 in the May final. Manufacturing

expected at 54.6 versus 55.1 and services at 51.0 versus 50.7, respectively.

US Richmond Fed Manufacturing Index for June (Tue

1000 EDT; Tue 1400 GMT)

Consensus Forecast, Index: 8

Consensus Range, Index: 7 to 8

Forecasters expect the index at 8 for June, down from 13.0

in May but still showing expansion in business activity.

Wednesday

Australia Monthly CPI for May (Wed 1130 AEST; Wed 0130

GMT; Tue 2130 EDT)

Consensus Forecast, Y/Y: 4.3%

Consensus Range, Y/Y: 3.8% to 4.9%

Food and housing prices expected to lift CPI while clothing

and footwear keep a lid on things. The consensus looks for CPI at 4.3 percent

on year on May versus 4.2 percent in April.

Germany Ifo Survey for June (Wed 1000 CEST; Wed 0800

GMT; Wed 0400 EDT)

Consensus Forecast, Business Climate: 85.5

Consensus Range, Business Climate: 84.2 to 85.8

Consensus Forecast, Current Conditions: 86.2

Consensus Range, Current Conditions: 85.5 to 86.3

Consensus Forecast, Business Expectations: 84.5

Consensus Range, Business Expectations: 83.0 to 85.2

Business climate index is seen improving to 85.5 in June

from 84.9 in May.

US Current Account Balance for First Quarter (Wed 0830

EDT; Wed 1230 GMT)

Consensus Forecast, $ Blns: -$227.0 B

Consensus Range, $ Blns: -$241.0 B to -$177.5 B

The current account gap is expected wider at $227 billion in

Q1 from $190.7 billion in Q4.

US New Home Sales for May (Wed 1000 EDT; Wed 1400

GMT)

Consensus Forecast, Annual Rate: 640K

Consensus Range, Annual Rate: 600K to 650K

Sales seen better at a 640K annual rate in May, up from 622K

in April.

Thursday

Australia Labour Force Survey for May (Thu 1130 AEST;

Thu 0130 GMT; Wed 2130 EDT)

Consensus Forecast, Employment - M/M: 33K

Consensus Range, Employment - M/M: 14K to 45K

Consensus Forecast, Unemployment Rate: 4.4%

Consensus Range, Unemployment Rate: 4.3% to 4.6%

After a surprising 19K drop in employment in April (many

blamed seasonal adjustment problems), jobs are expected to rebound by 33K in

May. The jobless rate is also expected to retreat to 4.4 percent in May from

4.5 percent in April.

Australia House Spending for May (Thu 1130 AEST; Thu 0130

GMT; Wed 2130 EDT)

Consensus Forecast, M/M: 0.5%

Consensus Range, M/M: -0.5% to 4.5%

Spending expected to rebound by 0.5 percent in May after

dropping by 1.1 percent on the month in April.

Germany GfK Consumer Climate for July (Thu 0800 CEST;

Thu 0600 GMT; Thu 0200 EDT)

Consensus Forecast, Index: -28.0

Consensus Range, Index: -30.0 to -26.5

The consensus sees the index higher but still gloomy at

minus 28.0 for July versus minus 29.8 in June.

US Durable Goods Orders for May (Thu 0830 EDT; Thu

1230 GMT)

Consensus Forecast, New Orders - M/M: -4.7%

Consensus Range, New Orders - M/M: -6.9% to -3.2%

Consensus Forecast, Ex-Transportation - M/M: 0.4%

Consensus Range, Ex-Transportation - M/M: 0.2% to 0.9%

Volatile aircraft orders seen hitting the headline figure,

down 4.7 percent on month. Ex-transportation expected to show decent 0.4

percent increase, with support from the AI buildout.

US GDP for First Quarter (Thu 0830 EDT; Thu 1230 GMT)

Consensus Forecast, Q/Q - Annual Rate: 1.6%

Consensus Range, Q/Q - Annual Rate: 1.3% to 2.5%

The final reading on Q1 GDP expected to show no revision

from growth at 1.6 percent reported last time.

US Jobless Claims for Week of June 20 (Thu 0830 EDT;

Thu 1230 GMT)

Consensus Forecast, Initial Claims - Level: 225 K

Consensus Range, Initial Claims - Level: 223 K to 240

K

Claims expected at 225K versus 226K last week, basically

steady in their recent range, which suggests ongoing balance in the job market.

US Personal Income and Outlays for May (Thu 0830 EDT;

Thu 1230 GMT)

Consensus Forecast, Personal Income - M/M: 0.4%

Consensus Range, Personal Income - M/M: 0.1% to 0.5%

Consensus Forecast, Personal Consumption Expenditures -

M/M: 0.5%

Consensus Range, Personal Consumption Expenditures - M/M:

0.2% to 0.7%

Consensus Forecast, PCE Price Index - M/M: 0.4%

Consensus Range, PCE Price Index - M/M: 0.4% to 0.5%

Consensus Forecast, PCE Price Index - Y/Y: 4.1%

Consensus Range, PCE Price Index - Y/Y: 4.0% to 4.1%

Consensus Forecast, Core PCE Price Index - M/M: 0.3%

Consensus Range, Core PCE Price Index - M/M: 0.2% to

0.4%

Consensus Forecast, Core PCE Price Index - Y/Y: 3.4%

Consensus Range, Core PCE Price Index - Y/Y: 3.3% to

3.5%

The core PCE prices index is seen at 0.3 percent on month

and 3.4 percent on year, based on CPI and PPI readings already released for

May. Consumers continue spending beyond growth in income with PCE seen up 0.5

percent and income seen at 0.4 percent in May.

Friday

Japan Tokyo CPI for May (Fri 0830 JST; Thu 2330 GMT;

Thu 1930 EDT)

Consensus Forecast, CPI - Y/Y: 1.7%

Consensus Range, CPI - Y/Y: 1.4% to 1.8%

Consensus Forecast, Ex-Fresh Food - Y/Y: 1.6%

Consensus Range, Ex-Fresh Food - Y/Y: 1.4% to 1.7%

Consensus Forecast, Ex-Fresh Food & Energy - Y/Y:

1.8%

Consensus Range, Ex-Fresh Food & Energy - Y/Y: 1.6%

to 1.9%

Tokyo's consumer price index, a leading indicator of the

national inflation trend, is expected to accelerate in June, reflecting higher

energy costs and supply concerns surrounding naphtha, other oil products and

chemicals amid the conflict involving the United States and Iran.

Core CPI, which excludes fresh food, is expected to

accelerate for the first time in eight months in June. The core CPI is forecast

to gain 1.6 percent on the year in June, up from a 1.3% increase in May, when

it recorded its slowest pace since March 2022. Core inflation has decelerated

sharply from the 3.6% rise posted in May 2025.

Despite easing food inflation, the impact of rising global

commodity prices is beginning to filter through to consumer prices. Government

measures to cap gasoline prices at around 170 per liter and the Tokyo

metropolitan government's decision to waive water charges for all households

during the summer are expected to help limit upward inflation pressure but are

unlikely to fully offset the impact of higher import costs.

The other key inflation measures are also expected to

advance. The overall CPI is forecast to increase 1.7 percent on the year in

June, compared with a 1.4 percent rise in May. The June level will be the

highest since December, when it posted a 2.0 percent rise. The core-core index,

which excludes both fresh food and energy, is expected to rise 1.8 percent, up

from 1.6 percent in May.

Singapore Industrial Production for May (Fri 1300 SGT;

Fri 0500 GMT; Fri 0100 EDT)

Consensus Forecast, Y/Y: 17.2%

Consensus Range, Y/Y: 17.2% to 28.0%

Output expected up 17.2 percent on year in May versus 17.6

percent in April.

Italy Business and Consumer Confidence for June

Consensus Forecast Manufacturing Business Confidence, Index:

88.5

Consensus Range, Manufacturing Business Confidence: 87.4

to 88.5

Consensus Forecast Consumer Confidence, Index: 93.0

Consensus Range, Consumer Confidence: 93.0 to 94.4

Manufacturing business confidence expected up to 88.5 in

June from 87.9 in May. Consumer confidence seen at 93.0 versus 93.4.

US International Trade in Goods (Advance) for May (Fri

0830 EDT; Fri 1230 GMT)

Consensus Forecast, Balance: - $85.2 B

Consensus Range, Balance: -$87.5 B to-$81.0 B

The goods trade gap is seen at $85.2 billion in May versus

$82.4 billion in April.

US Consumer Sentiment for June (Fri 1000 EDT; Fri

1400 GMT)

Consensus Forecast, Index: 49.9

Consensus Range, Index: 48.9 to 51.0

The consensus looks for an uptick in the sentiment index at

49.9 from 48.9 in May.

|

![[Apple App Store]](/images/AppleAppStore.png)

![[Econoday on Kindle]](/images/kindle.jpg)